- What is Cash Flow Statement?

- How to Prepare a Cash Flow Statement

- Indirect Method vs. Direct Method: What is the Difference?

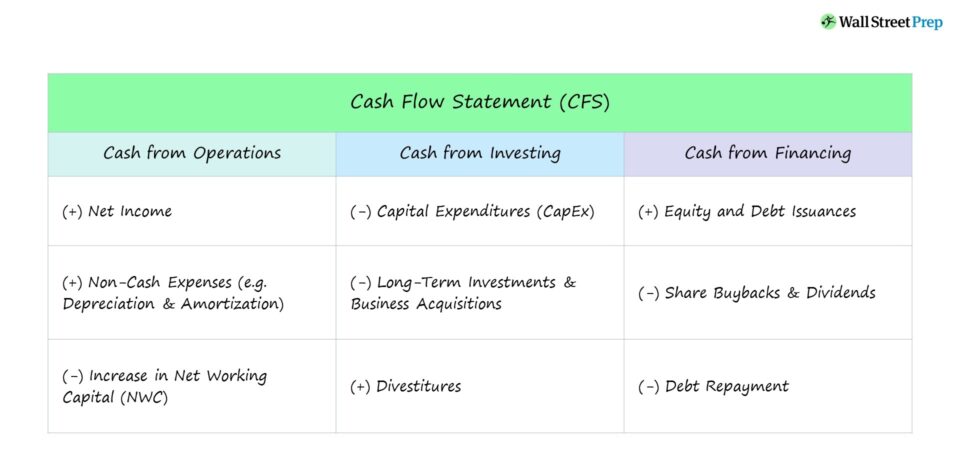

- What are the Components of the Cash Flow Statement?

- Cash Flow Statement Formula

- Cash Flow Statement Example: Apple (AAPL)

- How are the 3-Statements Linked?

- Cash Flow Statement Calculator — Excel Template

- 1. How to Build Cash Flow Statement in Excel

- 2. Income Statement Calculation Example (P&L)

- 3. Cash Flow Statement Calculation Example

- 4. Balance Sheet Calculation Example

What is Cash Flow Statement?

The Cash Flow Statement (CFS) is a financial statement that reconciles net income based on the actual cash inflows and outflows in a period.

Often used interchangeably with the term, “statement of cash flows,” the cash flow statement tracks the real inflows and outflows of cash from operating, investing and financing activities over a pre-defined period.

- The cash flow statement (CFS) is a financial report that details actual cash inflows and outflows over a specific period, reconciling net income with cash movements from operating, investing, and financing activities.

- There are two methods for preparing a cash flow statement: the indirect method, which adjusts net income for non-cash items and changes in working capital, and the direct method, which lists cash receipts and payments directly.

- The cash flow statement (CFS) consists of three main sections: Cash Flow from Operating Activities (CFO), Cash Flow from Investing Activities (CFI), and Cash Flow from Financing Activities (CFF), resulting in the net change in cash for the period (and ending cash balance).

- The cash flow statement (CFS) reconciles net income for discrepancies between accrual accounting profits and actual cash flows, addressing issues such as depreciation, stock-based compensation, and changes in working capital that can potentially be misleading.

How to Prepare a Cash Flow Statement

The cash flow statement (CFS), along with the income statement and balance sheet, represent the three core financial statements.

In accounting and finance, the cash flow statement (CFS), or “statement of cash flows,” matters because the financial statement reconciles the shortcomings of the reporting standards established under accrual accounting.

- Revenue Recognition (ASC 606) ➝ Under accrual accounting, revenue is recognized once the product/service is delivered to the customer (and “earned”), as opposed to when a cash payment is received (i.e. the revenue recognition principle).

- Matching Principle ➝ Based on the matching principle, expenses are incurred in the same period as the coinciding revenue to match the timing with the benefit.

- Non-Cash Items ➝ The depreciation expense is a common example of a non-cash item recorded on the income statement, despite the fact that the real cash outflow occurs in the initial year of the capital expenditure (Capex).

The net income as shown on the income statement – i.e. the accrual-based “bottom line” – can therefore be a misleading depiction of what is actually occurring to the company’s cash and profitability.

Therefore, the statement of cash flows is necessary to reconcile net income to adjust for factors that include the following:

- Depreciation and Amortization (D&A)

- Stock-Based Compensation (SBC)

- Changes in Working Capital (e.g. Accounts Receivable, Inventory, Accounts Payable, Accrued Expenses)

- One-Time Events

In effect, the real movement of cash during the period in question is captured on the statement of cash flows – which brings attention to operational weaknesses and investments/financing activities that do not appear on the accrual-based income statement.

The impact of non-cash add-backs is relatively straightforward, as these have a net positive impact on cash flows (e.g. tax savings).

However, for changes in net working capital, the following rules apply:

- Increase in NWC Asset and/or Decrease in NWC Liability ➝ Decrease in Cash Flow

- Increase in NWC Liability and/or Decrease in NWC Asset ➝ Increase in Cash Flow

Focusing on net income without looking at the real cash inflows and outflows can be misleading, because accrual-basis profits are easier to manipulate than cash-basis profits. In fact, a company with consistent net profits could potentially even go bankrupt.

Indirect Method vs. Direct Method: What is the Difference?

The two methods by which cash flow statements (CFS) can be presented are the indirect method and direct method.

| Format | Description |

|---|---|

| Indirect Method |

|

| Direct Method |

|

What are the Components of the Cash Flow Statement?

Under the indirect method, the format of the cash flow statement (CFS) comprises of three distinct sections.

| Format | Description |

|---|---|

| Cash Flow from Operating Activities (CFO) |

|

| Cash Flow from Investing Activities (CFI) |

|

| Cash Flow from Financing Activities (CFF) |

|

Cash Flow Statement Formula

If the three sections are added together, we arrive at the “Net Change in Cash” for the period.

Subsequently, the net change in cash amount will then be added to the beginning-of-period cash balance to calculate the end-of-period cash balance.

The shortcomings regarding the income statement (and accrual accounting) are addressed here by the CFS, which identifies the cash inflows and outflows over a certain time span while utilizing cash accounting—i.e. tracking the cash coming in and out of the company’s operations.

Cash Flow Statement Example: Apple (AAPL)

The following is a real world example of a cash flow statement prepared by Apple (NASDAQ: AAPL) prepared under GAAP accrual accounting standards.

Apple Cash Flow Statement Example (Source: AAPL 10-K)

How are the 3-Statements Linked?

Assuming the beginning and end of period balance sheets are available, the cash flow statement (CFS) could be put together—even if not explicitly provided—as long as the income statement is also available.

- Net Income ➝ Net income from the income statement flows in as the starting line item on the cash flow from operations section of the CFS.

- Change in NWC ➝ Net working capital (NWC) line items on the balance sheet are each tracked on the CFS.

- Capex and PP&E ➝ Cash outflows from the purchase of long-term fixed assets (PP&E) are accounted for in the capital expenditures (Capex) line item of the cash flow from investing section.

- Retained Earnings ➝ Issuance of common or preferred dividends are deducted from net income, with the remaining profits flowing into the retained earnings account.

- Debt and Equity Issuances ➝ Capital raising efforts, such as issuing debt or equity financing, are recorded in the cash flow from financing section.

- Ending Cash ➝ The ending cash balance stated on the cash flow statement becomes the cash balance recorded on the balance sheet for the current period.

Cash Flow Statement Calculator — Excel Template

We’ll now move to a modeling exercise, which you can access by filling out the form below.

1. How to Build Cash Flow Statement in Excel

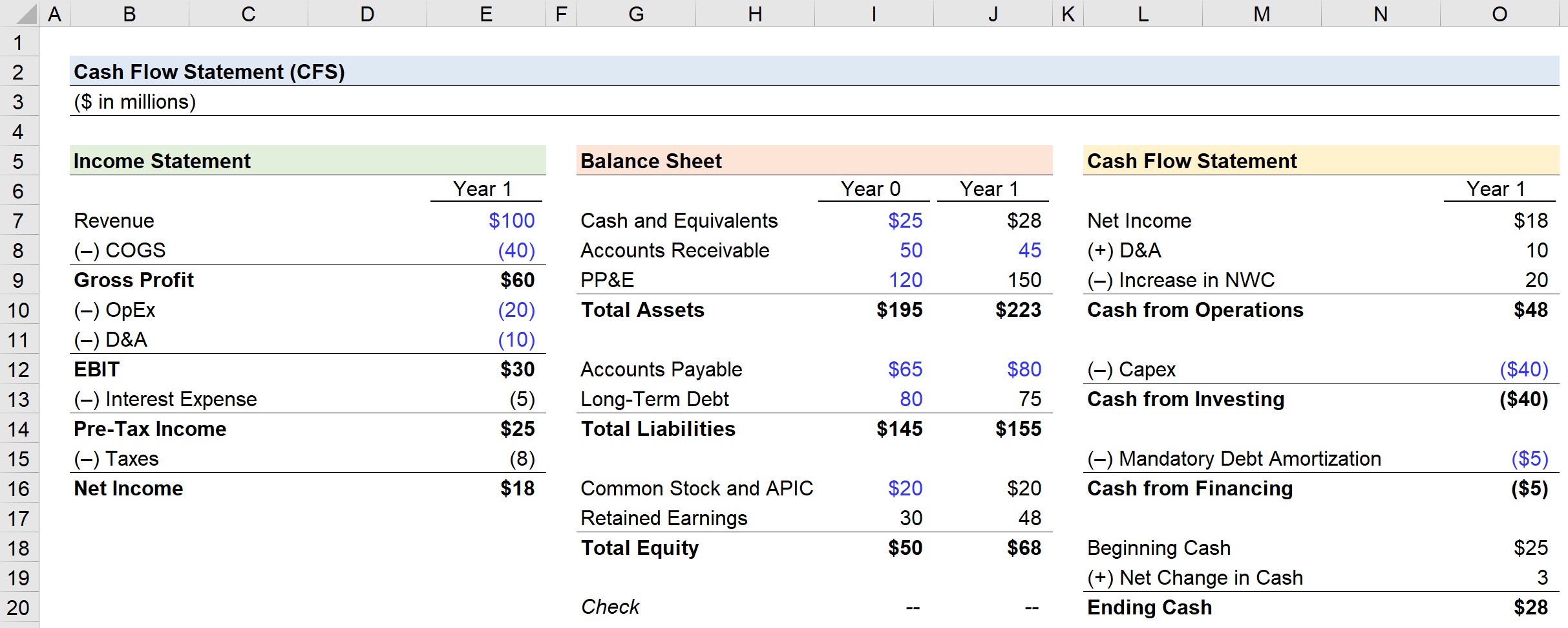

Suppose we are provided with the three financial statements of a company, including two years of financial data for the balance sheet.

The completed statement of cash flows, which we’ll work towards computing throughout our modeling exercise, can be found below.

2. Income Statement Calculation Example (P&L)

In Year 1, the income statement consists of the following assumptions.

| Income Statement (P&L) | Year 1 |

|---|---|

| Revenue | $100 million |

| COGS | ($40 million) |

| Gross Profit | $60 million |

| OpEx | ($20 million) |

| D&A | ($10 million) |

| EBIT | $30 million |

| Interest Expense (6%) | ($5 million) |

| Pre-Tax Income (EBT) | $25 million |

| Taxes @ 30% | ($8 million) |

| Net Income | $18 million |

3. Cash Flow Statement Calculation Example

The net income of $18m is the starting line item of the CFS.

In the “Cash from Operations” section, the two adjustments are the:

- (+) D&A: $10m

- (–) Increase in NWC: $20m

Next, the only line item in the “Cash from Investing” section is capital expenditures, which in Year 1 is assumed to be:

- (–) Capex: $40m

Likewise, the only “Cash from Financing” line item is the mandatory debt amortization (i.e. required pay down of debt principal):

- (–) Mandatory Debt Amortization: $5m

The beginning cash balance, which we get from the Year 0 balance sheet, is equal to $25m, and we add the net change in cash in Year 1 to calculate the ending cash balance.

- Cash from Operations: $48m

- (+) Cash from Investing: -$40m

- (+) Cash from Financing: -$5m

- Net Change in Cash: $3m

Upon adding the $3m net change in cash to the beginning balance of $25m, we calculate $28m as the ending cash.

- Beginning Cash: $25m

- (+) Net Change in Cash: $3m

- Ending Cash: $28m

4. Balance Sheet Calculation Example

On the Year 1 balance sheet, the $28m in ending cash that we just calculated on the CFS flows into the current period cash balance account.

For the working capital assets and liabilities, we assumed the YoY balances changed from:

- Accounts Receivable: $50m to $45m

- Accounts Payable: $65m to $80m

Operating assets declined by $5m while operating liabilities increased by $15m, so the net change in working capital is an increase of $20m – which our CFS calculated and factored into the cash balance calculation.

For our long-term assets, PP&E was $100m in Year 0, so the Year 1 value is calculated by adding Capex to the amount of the prior period PP&E and then subtracting depreciation.

- PP&E – Year 1: $100m + $40m – $10m = $110m

Next, our company’s long-term debt balance was assumed to be $80m, which is decreased by the mandatory debt amortization of $5m.

- Long-Term Debt – Year 1: $80m – $5m = $75m

With the assets and liabilities side of the balance sheet complete, all that remains is the shareholders’ equity side.

The common stock and additional paid-in capital (APIC) line items are not impacted by anything on the CFS, so we just extend the Year 0 amount of $20m to Year 1.

- Common Stock and APIC – Year 1: $20m

The formula in Year 0 of the retained earnings balance serves as a “plug” for the accounting equation to remain true (i.e. assets = liabilities + equity).

But for Year 1, the retained earnings balance is equal to the prior year’s balance plus net income.

- Retained Earnings – Year 1: $30m + $18m = $48m

Note that if there were any dividends issued to shareholders, the amount paid out would come out of retained earnings.

In our final step, we can confirm our model is built correctly by checking that both sides of our balance sheet in Year 0 and Year 1 are, in fact, in balance (i.e. Assets = Liabilities + Equity).

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today

hello, I am wondering why taxes of $8 were not deducted from the cash flow via the operating cashflows to get to $40 from the $48.

Hi, Gerald, The $8 of tax expense is already included in the net income of $18, which is the starting point of our CFO, so we do not need to subtract it again. However, non-cash items like D&A need to be added back to net income since they are non-cash… Read more »