- What is First Chicago Method?

- How Does the First Chicago Method Work?

- How to Calculate the First Chicago Method

- Scenario Planning: Base vs. Upside vs. Downside Case

- First Chicago Method Steps

- First Chicago Method: What are the Pros and Cons?

- First Chicago Method Calculator

- First Chicago Method Calculation Example

What is First Chicago Method?

The First Chicago Method is a probability-weighted valuation of a company using different cases and a probability weight assigned to each case.

How Does the First Chicago Method Work?

The First Chicago Method estimates the value of a company by taking the probability-weighted sum of three different valuation scenarios.

The method is most often used to value early-stage companies with unpredictable futures, such as venture-backed startups yet to turn a profit.

In practice, forecasting the performance of high-growth, early-stage companies to estimate the return on an early-stage investment could prove difficult because of the wide range of potential outcomes.

Hence, the First Chicago Method is an approach to valuation in which different scenarios are probability-weighted.

How to Calculate the First Chicago Method

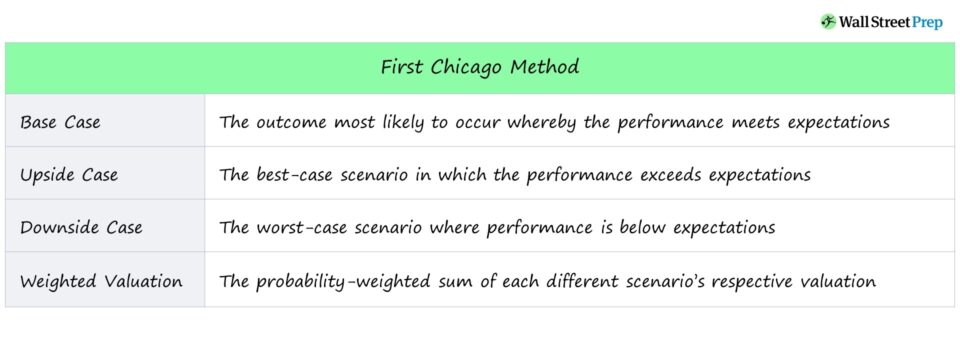

The three different scenarios consist of the following:

- Base Case → The outcome that is most likely to occur where performance meets expectations, so the highest probability weight is attached to this case.

- Upside Case → The best-case scenario in which the performance exceeds expectations, with usually the 2nd lowest probability of occurrence in most cases.

- Downside Case → The worst-case scenario where performance is below expectations, with typically the lowest probability of occurrence.

The value attributable to each case is commonly obtained from two valuation approaches:

- Discounted Cash Flow (DCF)

- Venture Capital Method (VC)

The estimated valuation will differ in each case because of the upward or downward adjustments to the underlying assumptions that impact the valuation.

The assumptions can differ in various ways, such as the discount rate, year-over-year (YoY) growth rates, comps used in determining the exit multiple, and more.

Scenario Planning: Base vs. Upside vs. Downside Case

The upside and downside cases are the two outcomes that are less likely to occur, with the latter usually being the lower likelihood of the two.

However, the reason is not that the worst-case scenario is less likely to happen, but rather that if the worst case has a higher likelihood of occurrence, it would not be worth considering an investment in the first place.

Depending on who is performing the analysis, additional cases with added contingencies could be added to the core three.

In venture investing, most investments are made with the expectation of failure, i.e., the “home runs” return the fund multiple times of their initial value and offset the losses incurred from the other failed investments.

In contrast, the base case represents the targeted performance (and returns) when integrating different cases into models for late-stage buyout investments and public equities markets.

Nevertheless, in the field of early to mid-stage investing (i.e., venture capital, growth equity), the end-goal is to exceed the base case by a substantial margin.

First Chicago Method Steps

Two other columns will be presented to the right once the three cases are listed in a table.

- Probability Weight (%) → The likelihood that the case is expected to occur out of all potential outcomes.

- Implied Valuation → The discounted cash flow (DCF) or VC Valuation Method derived value that corresponds to each case (Base, Upside, and Downside).

While it should go without saying, confirming that the sum of all probability weights equals 100% is still recommended.

Moreover, the probability weights assigned to the upside and downside cases are usually similar.

Once the table is all set, the final step is to multiply the probability of each case by the respective valuation amount, with the sum of all the values representing the concluded implied valuation.

First Chicago Method: What are the Pros and Cons?

| Advantages | Disadvantages |

|---|---|

|

|

|

|

|

|

First Chicago Method Calculator

We’ll now move to a modeling exercise, which you can access by filling out the form below.

First Chicago Method Calculation Example

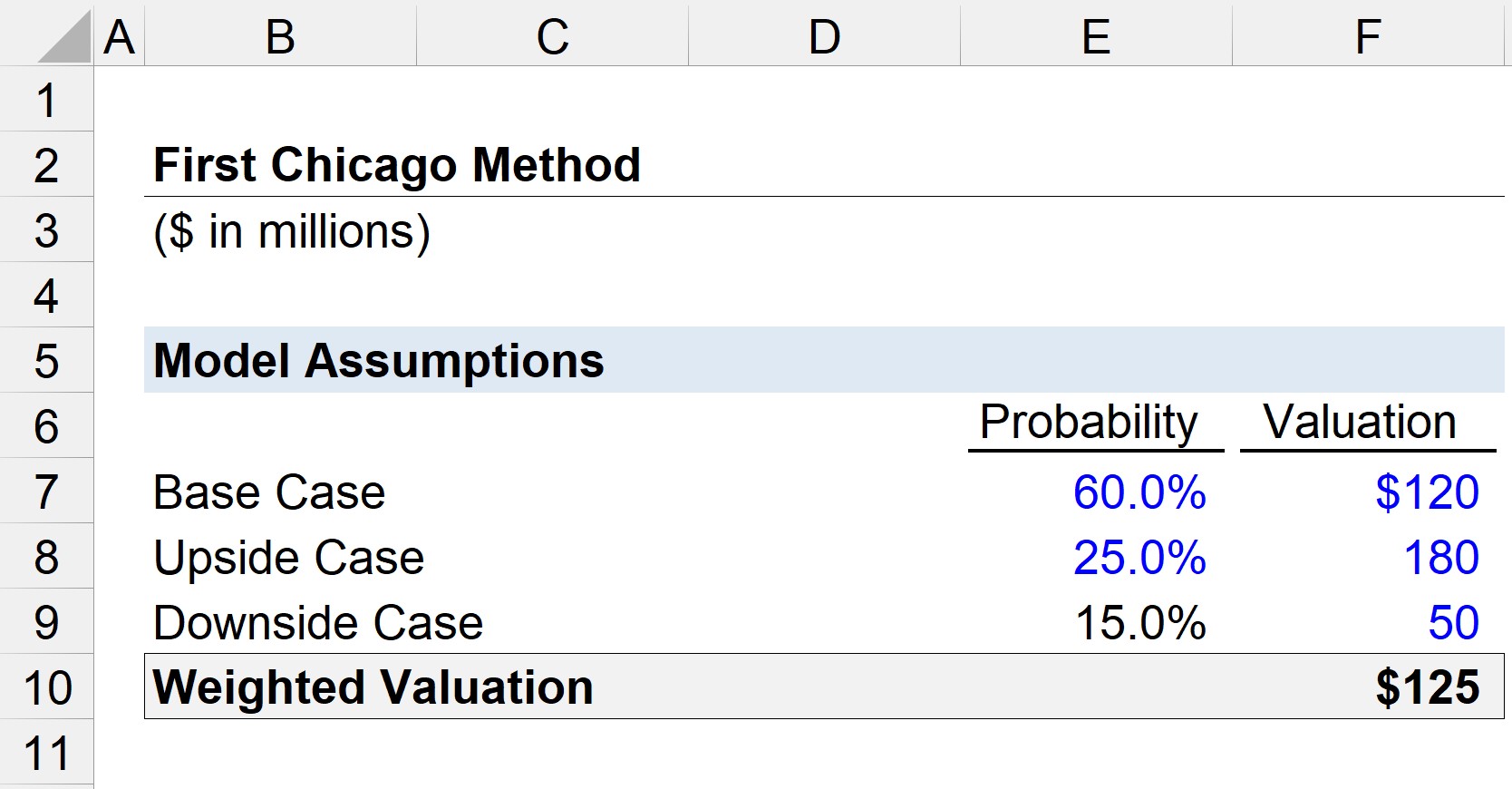

Suppose we are valuing a growth stage company using the First Chicago Method, with the DCF model already completed – each with a different set of assumptions.

Our DCF model of the company approximated the valuation of the company under three different scenarios:

- Base Case = $120 million

- Upside Case = $180 million

- Downside Case = $50 million

The probability weights for each case are determined as follows:

- Base Case = 60%

- Upside Case = 25%

- Downside Case = 15% (1 – 85%)

Using the “SUMPRODUCT” Excel function, with the first array comprising the probability weights and the second array of valuations, we arrive at a weighted valuation of $125 million.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today