Skip to main content

Skip to main content

- What is Multiple of Money?

- How to Calculate Multiple of Money (MoM)

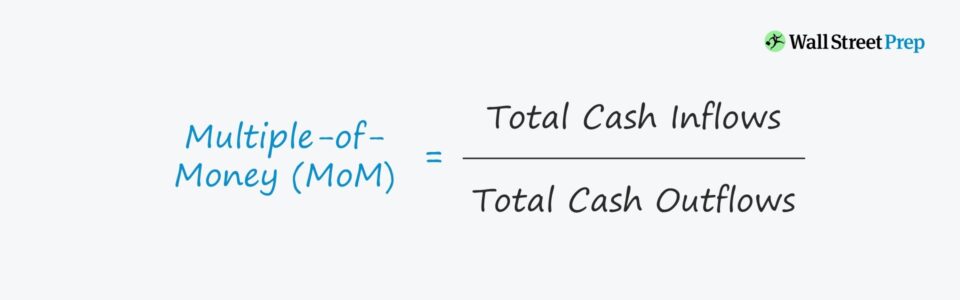

- Multiple of Money Formula (MoM)

- MoM to IRR Approximations

- Multiple of Money (MoM) vs. Internal Rate of Return (IRR)

- Multiple of Money Calculator (MoM)

- Step 1. LBO Model Returns Assumptions

- Step 2. Multiple of Money Calculation Example (MoM)

What is Multiple of Money?

The Multiple of Money (MoM) compares the amount of equity the sponsor takes out on the date of exit relative to their initial equity contribution.

Otherwise, referred to as the cash-on-cash return or multiple of invested capital (MOIC), the multiple of money (MoM) is one of the most widely used metrics for measuring the return on an investment as well as tracking the performance of a fund.

How to Calculate Multiple of Money (MoM)

The multiple of money (MoM) is a critical measure of returns in the private equity (PE) industry, alongside the internal rate of return (IRR).

Most often used in the context of a leveraged buyout (LBO), the multiple of money (MoM) is the ratio between 1) the total cash inflows received and 2) the total cash outflows from the perspective of the investor, i.e. the financial sponsor.

- Cash Inflows: Sale Proceeds, Management Fees, Shareholder Dividends

- Cash Outflows: Purchase Price (i.e. Initial Outlay)

Multiple of Money Formula (MoM)

The formula to calculate the multiple of money (MoM) is as follows.

For example, if the total cash inflows (i.e. proceeds from the sale of a portfolio company) are $100m from a $10m initial equity investment, the MoM would be 10.0x.

- Multiple of Money (MoM) = $100 million ÷ $10 million = 10.0x

If given the multiple of money (MoM) of a particular investment, the internal rate of return (IRR) can be computed using the formula below.

The Wharton Online and Wall Street Prep Private Equity Certificate Program

Level up your career with the world's most recognized private equity investing program. Enrollment is open for the upcoming cohort.

Enroll TodayMoM to IRR Approximations

The following list contains the most common MoM to IRR approximations, which we recommend memorizing for those recruiting for roles in private equity.

- 2.0x MoM in 3 Years → ~25% IRR

- 2.0x MoM in 5 Years → ~15% IRR

- 2.5x MoM in 3 Years → ~35% IRR

- 2.5x MoM in 5 Years → ~20% IRR

- 3.0x MoM in 3 Years → ~45% IRR

- 3.0x MoM in 5 Years → ~25% IRR

Multiple of Money (MoM) vs. Internal Rate of Return (IRR)

- Neglects Time Value of Money (TVM): The multiple of money (MoM) metric cannot be used by itself due to the fact that it fails to consider the time value of money. For instance, a 2.0x multiple could be sufficient for certain funds if achieved within three years. But that might no longer be the case if receiving those proceeds took ten years instead.

- Less Time Consuming: Compared to the internal rate of return (IRR), calculating the MoM tends to be far less time-consuming because the metric quantifies “how much” the gross return was, as opposed to “when,” since time is not factored into the MoM formula.

- Non-Time Weighted Metric: The internal rate of return (IRR) metric takes into account both the amount received and the timing of when the proceeds were received. However, this causes the metric to be skewed at times due to attaching more weight to proceeds received earlier in time.

- Independent of Holding Period: For shorter time frames, the multiple of money (MoM) is arguably more important than the internal rate of return (IRR) – yet, for longer time horizons, achieving a higher IRR can be of greater important.

Multiple of Money Calculator (MoM)

We’ll now move to a modeling exercise, which you can access by filling out the form below.

Step 1. LBO Model Returns Assumptions

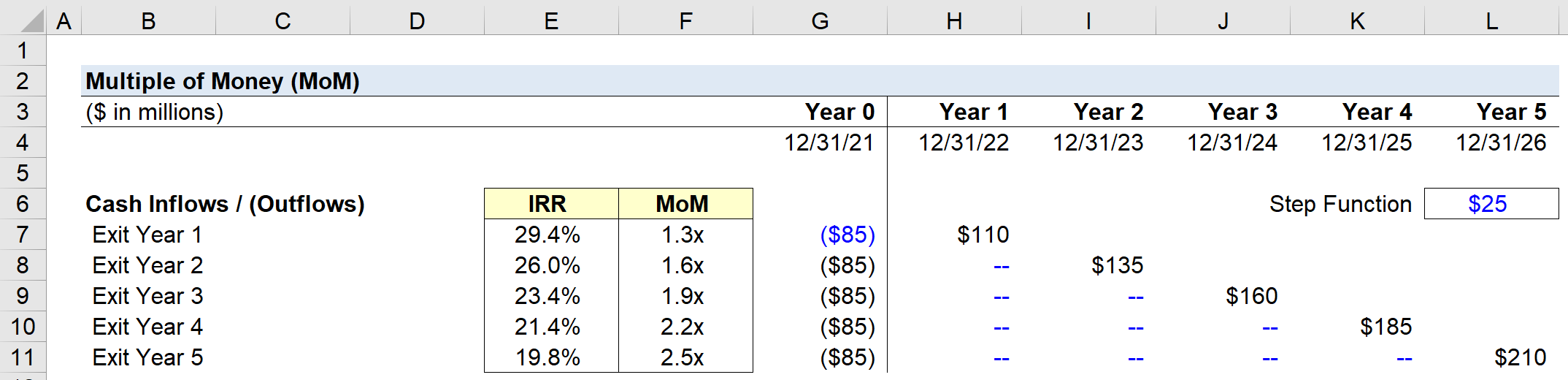

Suppose a private equity firm made an investment in Year 0 sized at $85m. The $85m will remain constant since regardless of when the firm decides to exit the investment, the value of the initial investment remains unchanged.

- Initial Investment (Year 0) = $85 million

We must also place a negative sign in front of the number because the initial investment represents an outflow of cash.

On the other hand, the positive cash inflows related to the exit proceeds are entered as positive integers, because those cash flows represent the proceeds distributed to the investor post-exit.

In our model, we are assuming that each year, the exit proceeds will increase by +$25m, starting from the initial investment amount of $85m.

- Exit Proceeds, Step Function = +$25 million

Therefore, the exit proceeds in Year 1 are $110m while in Year 5, the proceeds come out to $210m.

For the return calculation to be accurate, the table must display all the cash inflows and outflows, but most notably, the following two components:

- Initial Cash Outlay in Year 0 (i.e. Initial Purchase Price @ LBO)

- Exit Proceeds at Various Potential Exit Dates

In our simple LBO model, the two major expenditures and inflows of cash are the entry investment and the exit sale proceeds.

However, other inflows such as dividends or monitoring fees (i.e., portfolio company consulting) must also be accounted for (and entered as positive figures).

Step 2. Multiple of Money Calculation Example (MoM)

To calculate the MoM, we first sum up the cash inflows from the relevant year and then divide the amount by the cash outflow in Year 0 for each year.

If we assume the financial sponsor liquidated the investment in Year 5 (e.g. secondary buyout, sale to strategic, or IPO), the exit proceeds of $210m are divided by $85m (with a negative sign in front) to get to a 2.5x MoM.

Once the process is completed for each year, from our completed model, we can see the Year 5 IRR comes out to ~19.8% whereas the MoM comes out to ~2.5x.

- Internal Rate of Return (IRR), Exit Year 5 = 19.8%

- Multiple of Money (MoM), Exit Year 5 = 2.5x

")