- What is Operating Cash Flow?

- How to Calculate Operating Cash Flow (OCF)

- Operating Cash Flow Formula (Indirect Method)

- Operating Cash Flow Formula (Direct Method)

- OCF vs. FCF: What is the Difference?

- Operating Cash Flow Calculator (OCF)

- 1. Financial Assumptions

- 2. Operating Cash Flow Calculation Example (Indirect Method)

- 3. Operating Cash Flow Calculation Example (Direct Method)

What is Operating Cash Flow?

Operating Cash Flow (OCF) measures the net cash generated from the core operations of a company within a specified time period.

How to Calculate Operating Cash Flow (OCF)

OCF, short for “Operating Cash Flow,” refers to the net amount of cash brought in by a company’s day-to-day operations.

The income statement is reported per accounting standards established by U.S. GAAP, which has its shortcomings in reflecting the actual liquidity (i.e. cash on hand) of companies.

Hence, the cash flow statement (CFS) is necessary to understand the real cash inflows / (outflows) from operating, investing, and financing activities.

The CFS starts with the “Cash Flow from Operating Activities” section, which calculates a company’s operating cash flow (OCF) in a specified period.

The more operating cash flow (OCF) generated by a company, the more discretionary cash flow is available for investing and financing needs – all else being equal.

- Positive Operating Cash Flow (OCF) → Greater Discretionary Free Cash Flow (FCF)

- Negative Operating Cash Flow (OCF) → Less Discretionary Free Cash Flow (FCF)

In a scenario with positive OCF, the company’s operations generate adequate cash to meet its reinvestment needs, e.g. working capital and capital expenditures (CapEx).

But in the latter case with negative OCF, the company must seek external financing sources to meet its reinvestment spending needs, e.g. via equity and debt issuances.

The cash flow statement (CFS) can be presented under two methods — the indirect or the direct method:

- Indirect Method → The beginning line item is net income, which is adjusted for non-cash items (e.g. D&A) and changes in working capital to arrive at cash flow from operations.

- Direct Method → Instead of starting with net income, the direct method uses cash accounting to track the cash received from customers and paid out to third parties (e.g. suppliers, vendors).

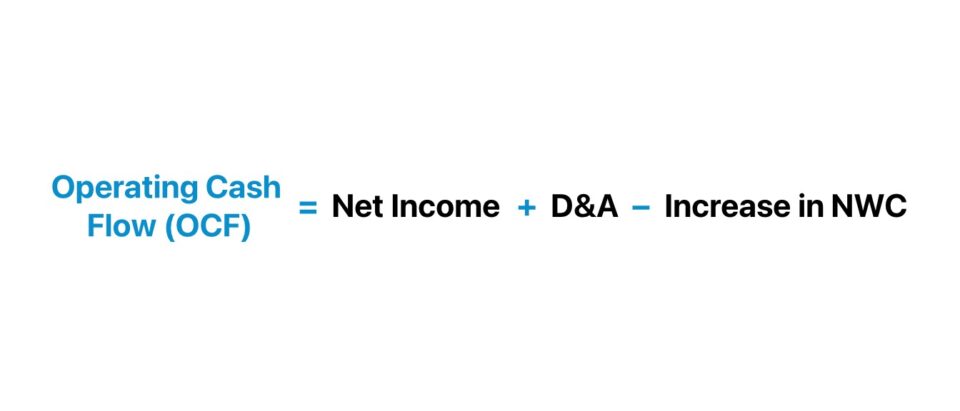

Operating Cash Flow Formula (Indirect Method)

Under the indirect method — the more common approach in the U.S. — the CFS’s top-line item is the accrual-based net income.

- The starting line item, net income (the “bottom line”), is first adjusted by adding back non-cash expenses (e.g. such D&A, stock-based compensation).

- Then, other adjustments are made for the changes in working capital.

- The CFO section converts the accrual-based net income metric by adjusting it for non-cash items (e.g. depreciation, amortization) and changes in net working capital (NWC).

- Once those adjustments have been made, the resulting line item is the “Cash Flow from Operating Activities”, i.e. the operating cash flow (OCF).

Upon consolidating the steps stated above, we can derive the formula to calculate operating cash flow (OCF).

The formula to calculate operating cash flow (OCF) adjusts net income by non-cash items like depreciation and amortization, and then the change in net working capital (NWC).

If OCF deviates substantially from net income, it implies further analysis is necessary to understand the underlying factors that are causing the difference.

The relationship between changes in working capital items and their respective cash flow impacts is described below:

- Increase in Working Capital Asset → Cash Outflow (”Use”)

- Decrease in Working Capital Asset → Cash Inflow (”Source”)

- Increase in Working Capital Liability → Cash Inflow (”Source”)

- Decrease in Working Capital Liability → Cash Outflow (”Use”)

| Working Capital Assets | Working Capital Liabilities |

|---|---|

For instance, if OCF is much lower than net income because of rising accounts receivable (A/R) — i.e. the sales in which customers paid on credit rather than cash — the company might have to reconsider how it collects cash payments from customers.

Operating Cash Flow Formula (Direct Method)

The less prevalent approach to calculating OCF is the direct method, which uses cash accounting to track the movement of cash during a specified period.

Compared to the indirect method, the direct method is simpler, as the formula comprises subtracting cash operating expenses from cash revenue.

To emphasize, only cash revenue and cash operating expenses are included under the direct method.

OCF vs. FCF: What is the Difference?

OCF differs from FCF because the calculation of FCF includes capital expenditures (Capex), unlike OCF.

Operating cash flow (OCF) and free cash flow (FCF) are both metrics used to assess the financial stability of a company, typically to determine if the cash generated is enough to meet its spending needs.

While there are several variations of calculating free cash flow (FCF) — namely, free cash flow to firm (FCFF) and free cash flow to equity (FCFE) — the simplest formula subtracts capital expenditures (Capex) from cash from operations (CFO).

The distinction between FCF and CFO is that FCF also deducts Capex, as it is a major cash outflow that is a core part of a company’s ability to produce cash flows.

For either metric, the higher the amount, the better off the company is (and vice versa), but FCF goes an extra step by considering Capex.

Operating Cash Flow Calculator (OCF)

We’ll now move to a modeling exercise, which you can access by filling out the form below.

1. Financial Assumptions

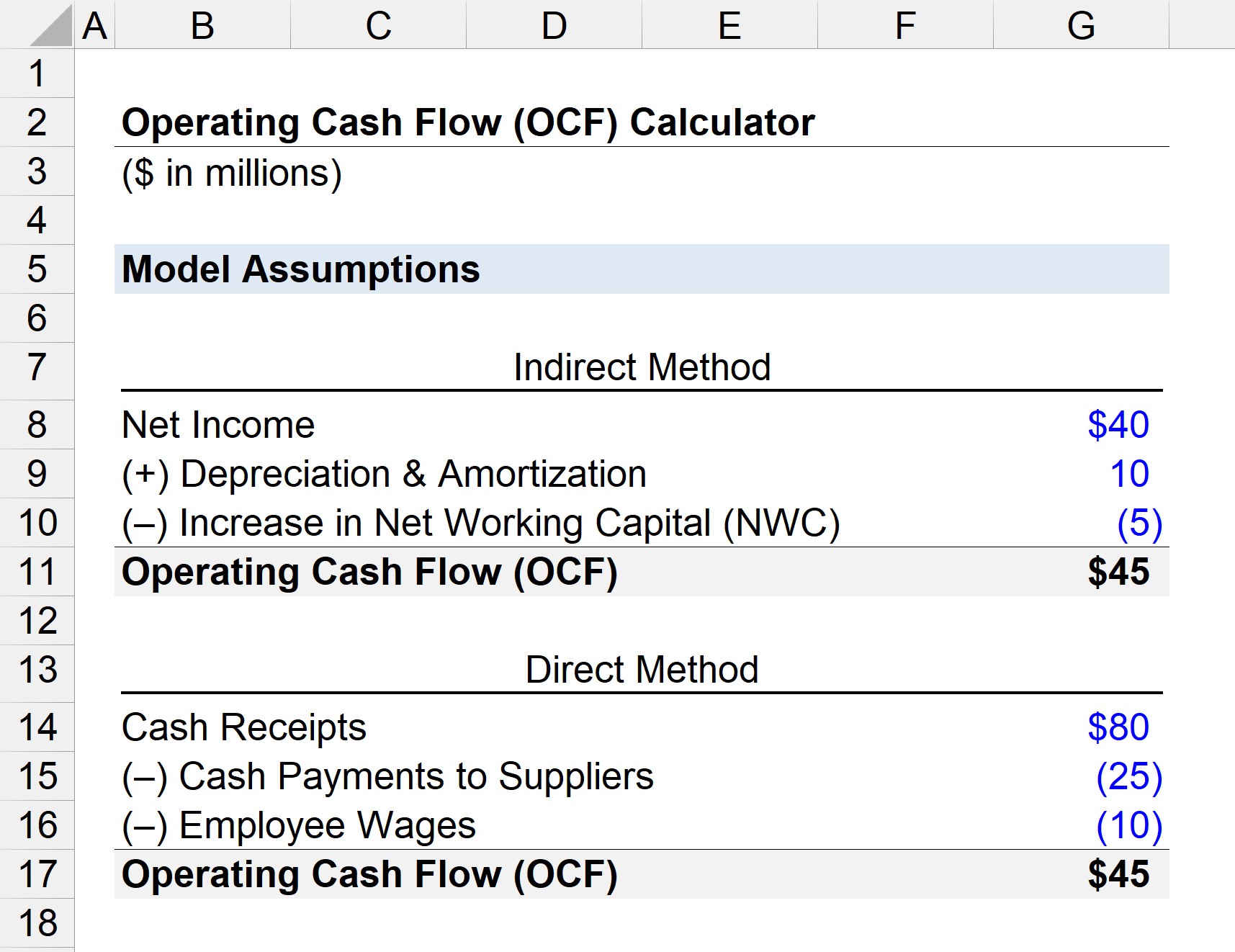

Suppose we’re tasked with calculating a company’s operating cash flow (OCF) in a given period with the following financial data.

Financial Data

- Net Income = $40 million

- Depreciation and Amortization (D&A) = $10 million

- Increase in Net Working Capital (NWC) = –$5 million

Our starting point is the net income metric, i.e. the accrual accounting profits of our company, which is derived from the income statement (the “bottom line”).

The depreciation and amortization expense, or “D&A”, is embedded within COGS and operating expense section.

D&A is a non-cash add-back because the real cash outflow via Capex already occurred in the initial period of purchase, so the cash flow impact is positive.

An increase in NWC reflects that there is more cash tied up in operations; thereby the cash flow decreases (i.e. a “use” of cash).

In contrast, a decrease in NWC represents an inflow of cash (i.e. a “source” of cash).

2. Operating Cash Flow Calculation Example (Indirect Method)

If we enter those assumptions into the OCF formula under the indirect method, we arrive at $45 million as our illustrative company’s OCF.

- Operating Cash Flow (OCF) = $40 million + $10 million – $5 million = $45 million

In short, the greater the variance between a company operating cash flow (OCF) and recorded net income, the more its financial statements (and operating results) are impacted by accrual accounting.

3. Operating Cash Flow Calculation Example (Direct Method)

In the next part of our modeling exercise, we’ll calculate OCF using the direct method.

Here, we’ll utilize the following assumptions:

- Cash Receipts = $80 million

- Cash Payments to Suppliers = –$25 million

- Employee Wages = –$10 million

Cash receipts refer to the cash payments received from customers, and the two cash operating expenses (i.e. cash reductions) consist of the following:

- Supplier Payments

- Employee Wages

Upon entering the assumptions into our OCF formula under the direct method, our company’s OCF is $45 million.

- Operating Cash Flow (OCF) = $80 million – $25 million – $10 million = $45 million

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today

This was very helpful.

Thanks, Fredy, glad to hear it!