Skip to main content

Skip to main content

- What is Break-Even Point?

- How to Calculate Break-Even Point (BEP)

- Break-Even Point Formula

- How to Conduct Break-Even Analysis

- Break Even Point Calculation Example (BEP)

- Break-Even Point Calculator (BEP)

- 1. Unit Economics and Cost Structure Assumptions

- 2. Goal Seek Function in Excel

- 3. Break-Even Analysis Example

What is Break-Even Point?

The Break-Even Point (BEP) is the inflection point at which the revenue output of a company is equal to its total costs and starts to generate a profit.

How to Calculate Break-Even Point (BEP)

There is no net loss or gain at the break-even point (BEP), but the company is now operating at a profit from that point onward.

For all business owners, particularly during the earlier stages of a business, one of the most crucial questions to answer is: “When will my business break even?”

Businesses share the similar core objective of eventually becoming profitable in order to continue operating. Otherwise, the business will need to wind-down since the current business model is not sustainable.

An unprofitable business eventually runs out of cash on hand, and its operations can no longer be sustained (e.g., compensating employees, purchasing inventory, paying office rent on time).

By understanding the required output to break even, a company can set revenue targets accordingly, as well as adjust its business strategy such as the pricing of its products/services and how it chooses to allocate its capital.

The steps to calculate the break-even point are as follows:

- Step 1 ➝ Calculate Sum of Fixed Costs

- Step 2 ➝ Calculate Contribution Margin

- Step 3 ➝ Divide Fixed Costs by Contribution Margin

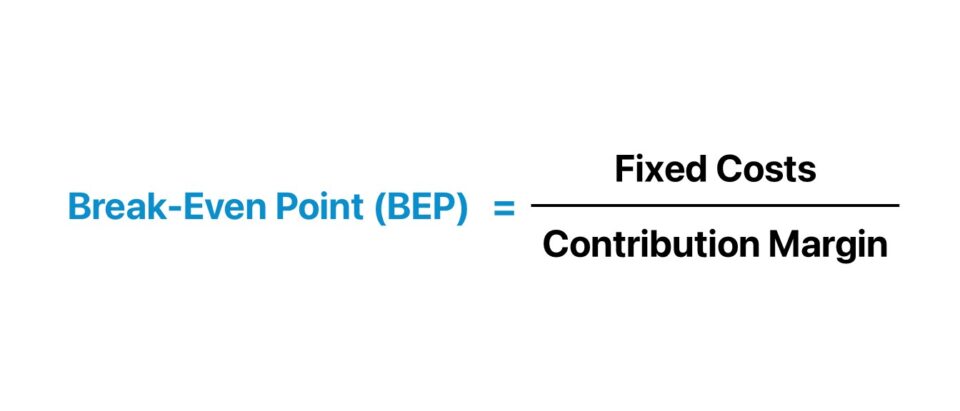

Break-Even Point Formula

The formula for calculating the break-even point (BEP) involves taking the total fixed costs and dividing the amount by the contribution margin per unit.

The contribution margin is the selling price per unit minus the variable costs per unit, and represents the amount of revenue remaining after meeting all the associated variable costs accumulated to generate that revenue.

- Contribution Margin = Fixed Costs ➝ If a company’s contribution margin (in dollar terms) is equal to its fixed costs, the company is at its break-even point.

- Contribution Margin > Fixed Costs ➝ If the company’s contribution margin exceeds its fixed costs, then the company actually starts profiting from the sale of its products or services.

How to Conduct Break-Even Analysis

If a company has reached its break-even point, the company is operating at neither a net loss nor a net gain (i.e. “broken even”).

The incremental revenue beyond the break-even point (BEP) contributes toward the accumulation of more profits for the company.

Conducting a break-even analysis is a prerequisite to setting prices appropriately, establishing clear and logical sales target goals, and identifying weaknesses in the current state of the business model that could benefit from improvements (e.g., sales tactics and marketing strategies).

Furthermore, established companies with a diverse portfolio of product/service offerings can estimate the break-even point on an individualized product-level basis to assess whether adding a certain product would be economically viable.

In effect, the insights derived from performing break-even analysis enables a company’s management team to set more concrete sales goals since a specific number to target was determined.

The Wharton Online & Wall Street Prep Applied Value Investing Certificate Program

Learn how institutional investors identify high-potential undervalued stocks. Enrollment is open for the upcoming cohort.

Enroll TodayBreak Even Point Calculation Example (BEP)

For example, if a company has $10,000 in fixed costs per month, and their product has an average selling price (ASP) of $100, and the variable cost is $20 for each product, that comes out to a contribution margin per unit of $80.

- Fixed Costs per Month = $10,000

- Average Selling Price (ASP) = $100.00

- Variable Cost per Unit = $20.00

- Contribution Margin = $80.00

Then, by dividing $10k in fixed costs by the $80 contribution margin, we arrive at approximately 125 units as the break-even point, meaning that if the company sells 125 units of its product, it’ll have made $0 in net profit.

- Break-Even Point (BEP) = 125 Units

Or, if using Excel, the break-even point can be calculated using the “Goal Seek” function.

After entering the end result being solved for (i.e., the net profit of zero), the tool determines the value of the variable (i.e., the number of units that must be sold) that makes the equation true.

Break-Even Point Calculator (BEP)

We’ll now move to a modeling exercise, which you can access by filling out the form below.

1. Unit Economics and Cost Structure Assumptions

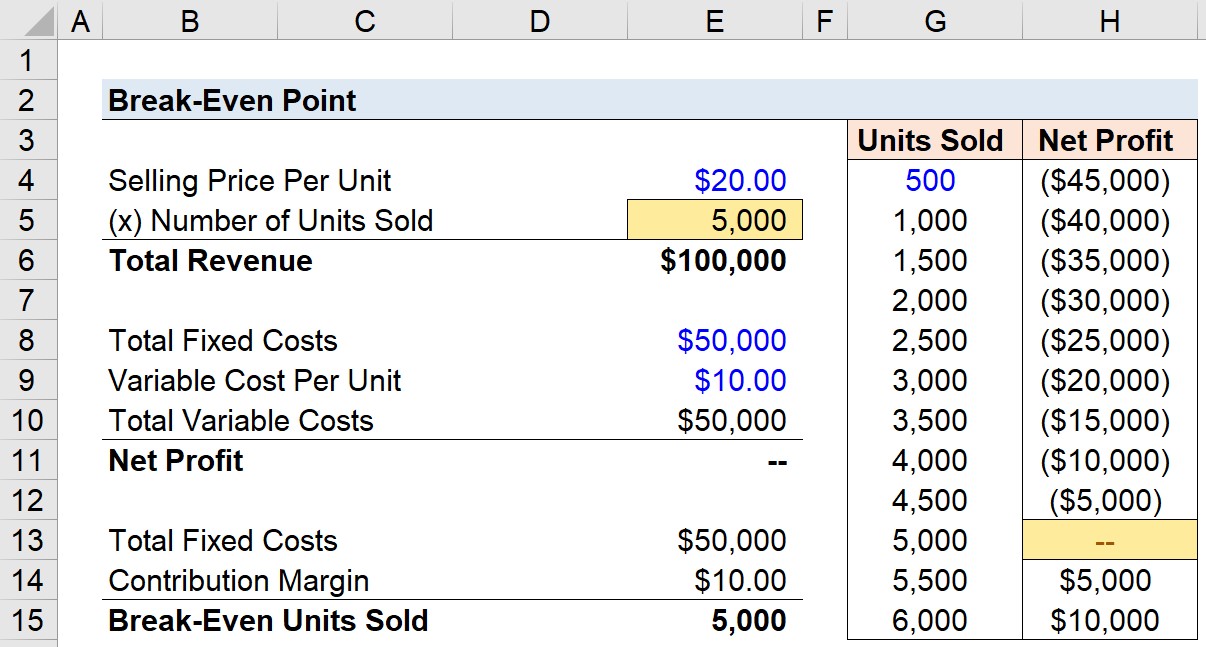

Let’s say that we have a company that sells products priced at $20.00 per unit, so revenue will be equal to the number of units sold multiplied by the $20.00 price tag.

- Selling Price Per Unit = $20.00

In terms of its cost structure, the company has fixed costs (i.e., constant regardless of production volume) that amounts to $50k per year. Recall, fixed costs are independent of the sales volume for the given period, and include costs such as the monthly rent, the base employee salaries, and insurance.

- Total Fixed Costs = $50,000

Moving onto our final assumption, the variable costs directly associated with the production of the products being sold are $10.00.

- Variable Costs = $10.00 Per Unit

In contrast to fixed costs, variable costs increase (or decrease) based on the number of units sold. If customer demand and sales are higher for the company in a certain period, its variable costs will also move in the same direction and increase (and vice versa).

The total variable costs will therefore be equal to the variable cost per unit of $10.00 multiplied by the number of units sold.

2. Goal Seek Function in Excel

We now have the assumptions in place to use the “Goal Seek” function in Excel (Alt ➝ A ➝ W ➝ G).

- Step 1 → First, we link to the net profit cell for the “Set cell” selection

- Step 2 → In the subsequent step, we are going to input zero as the “To value” since the profit we are targeting is $0 (i.e., the break-even point)

- Step 3 → Lastly, the “By changing cell” will be set to the number of units sold, as this is the variable that Excel will be adjusting until our target profit value is met

Upon doing so, the number of units sold cell changes to 5,000, and our net profit is equal to zero.

3. Break-Even Analysis Example

Quantifying the required number of units to be sold to have a net profit of zero was our intended goal, which in this particular scenario, the company must sell 5k units of its products to break even and start to generate a profit from its operations.

As we can see from the sensitivity table, the company operates at a loss until it begins to sell products in quantities in excess of 5k. For instance, if the company sells 5.5k products, its net profit is $5k.

Alternatively, the break-even point can also be calculated by dividing the fixed costs by the contribution margin.

The total fixed costs are $50k, and the contribution margin ($) is the difference between the selling price per unit and the variable cost per unit. So, after deducting $10.00 from $20.00, the contribution margin comes out to $10.00.

- Contribution Margin = $20.00 – $10.00 = $10.00

In conclusion, just like the output for the goal seek approach in Excel, the implied units needed to be sold for the company to break even come out to 5k.

- Break-Even Point = 5,000 Units Sold

How to find the BREAK EVEN POINT IN UNIT

IF THE GIVEN IS HERE

SALE – $1,100,000

TOTAL FIXED COST – 280,000

TOTAL VARIABLE COST – 660,000

UNIT PRICE – 40

WHAT IS THE BREAK EVEN POINT IN UNIT

Hi, Conan,

You would need 17,500 units to break even (1,100,000 / $40 = 27,500; 660,000 / 27,500 = $24 cost per unit; $40 – 24 = $16 profit per unit; 280,000 / $16 = 17,500 units to break even).

BB

Realy appreciated

You’re welcome!

Well understand

what are the formulas for break-even variable cost and break-even fixed cost?

Hi, Hamish, Do you mean the $ value of breakeven, not the number of units? For breakeven variable costs, if fixed costs are truly fixed and the units are given, you would use: revenue per unit – fixed costs / units. Fixed cost breakeven if variable costs per unit and… Read more »

kindly would like to know how to calculate the break even points given the variable cost,fixed cost and the net profit only

Hi, Nicholas,

You would not be able to calculate the break-even quantity of units unless you have revenue and variable cost per unit.

Brad

if Fixed cost , variable cost and sales amount available in profit and loss account , how to calculate bep amount with out units. with the help of profit and loss account

Hi, Sandes,

You have to have per unit data to calculate the breakeven point for fixed costs.

BB

May you please help me on this question. A company manufactures and sells a product for $20. The summarised income statement for year end is as follows: Sales $800 000 Direct Materials (120 000) Direct wages (160 000) Variable production O/H (80 000) Fixed production O/H (100 000) Fixed Administration O/H… Read more »

Hi, Greg, You need to add up the fixed expenses, and then divide that by the gross profit per unit (800K/20 for units) to get breakeven # of units. Then figure out how many more units need to be sold to get after-tax profit of $150K (divide that by 1… Read more »

Please help me calculate this A car has the following costs It makes 10 cars per week (figures in kshs) Rent-150000 per week Salaries -200000 per week Interest-50000 per week Materials -3000000 per car Wages-50000 per car Powers-25000 per car Sales commission -250000 per car If each car is sold… Read more »

Hi, Teresa,

If materials, wages, powers, and commission come to 625K total, and the cars are sold for 500K, then it seems like you are losing money on each car.

BB

If i have

Total units to be produced = 12000

Cost per unit = $37.40

Unit selling price = $53.98

Total Fixed Cost $35038

BEP = ?

How do i solve this problem?

What is the contribution Margin

Hi, Hussein,

Take the fixed costs and divide by the difference between the selling price and cost per unit ($16.58), and that will tell you how many units have to be sold to break even.

BB

What about if you have a large sum of products.

Hi, Ashraf,

If you have different products, then different mixes of product volume will be possible to achieve break even. If you can allocate fixed costs to each product line, then you can calculate break even for each of them.

BB

Hi Hussein

Only 2,189.8 units are needed to break even

Hi, Chuol,

Thanks for offering an answer. But how do you arrive at 2189.8, when fixed costs are $35,038 and the difference between selling price and cost per unit is $16.58?

BB

What is break even point sales determine algebrically and graphically

Hi, Sarwar, I suppose if you wanted to graph it, you would put $ on the y axis and units sold on the x axis, and label the amount of fixed costs on the y axis, then the number of units sold * the income per unit would represent a… Read more »

if i have

Total units to be produced = 4,500

Cost per unit = $12.40

Unit selling price = $21.98

Total Costs = $

BEP =

how do i solve this problem

Hi, Ivana,

To calculate BEP, you also need the amount of fixed costs that needs to be covered by the break-even units sold.

BB

No, need fixed cost

Hi, Alihamza,

Are you saying that Ivana does not need fixed costs, or that she does? The latter is true, she must have fixed costs to calculate break even.

BB

How can we quickly construct the sensitivity table in Column G and Column H?

Hi, Angel,

You could do a one-way data table, where you reference net income (E11) as the output variable in H3, and then you specify E5 as the column input (highlighting G3:H15 as your table).

BB

is it possible to use the “average” cost per unit in the BEP formula?

Hi, Erwin,

Yes, you would want to use the average cost per unit along with the average selling price to get the contribution margin per unit in the formula.

BB

How to find higher or lower bep

Hi, Lozita, I am not sure what you mean asking how to find higher or lower BEP. The point of this is to find out how many units must be sold to breakeven, and that is based on the gross profit of each unit sold and the amount of fixed… Read more »

Profit when sale are 40000

Fixed exp 8000

BEP 20000

Hi, Shadab,

What we mean here by BEP is the number of units that must be sold to just cover fixed costs so you would need to specify the revenue and variable costs per unit in order to know the BEP for fixed costs of 8000.

BB

fixed costs are costs required to cover the regular monthly expense. this means it does not include costs of machinery,land building,licence

Hi, Gabeini,

What we mean here by fixed costs are costs that are constant regardless of production volume, so we cannot arbitrarily declare that they only mean ‘regular monthly expenses’ and do not include those other line items, in case those items are constant regardless of volume.

BB

what are the formulas of BEP

Hi, Abraham, Do you mean the $ value of breakeven? For breakeven variable costs, if fixed costs are truly fixed and the units are given, you would use: revenue per unit – fixed costs / units. Fixed cost breakeven if variable costs per unit and units are given would be:… Read more »