- What is Reinvestment Rate?

- How to Calculate Reinvestment Rate

- Reinvestment Rate Formula

- What is a Good Reinvestment Rate?

- How Do Reinvestment Rate Impact Expected EBIT Growth?

- Reinvestment Rate Calculator | Excel Template

- 1. Capex, Depreciation and Working Capital Assumptions

- 2. Reinvestment Rate Calculation Example

What is Reinvestment Rate?

The Reinvestment Rate measures the percentage of a company’s after-tax operating income (i.e. NOPAT) that is allocated to capital expenditures (Capex) and net working capital (NWC).

How to Calculate Reinvestment Rate

The expected growth rate in operating income is a byproduct of the reinvestment rate and the return on invested capital (ROIC).

- Reinvestment Rate → The proportion of NOPAT re-invested into capital expenditures (Capex) and net working capital (NWC).

- Return on Invested Capital (ROIC) → The profitability percentage earned by a company using its equity and debt capital.

The calculation of the rate of a company’s reinvestment is a three-step process:

- First, we calculate net Capex, which is equal to capital expenditures minus depreciation.

- Next, the change in net working capital (NWC) is added to the result from the prior step, representing the dollar amount of reinvestment.

- Lastly, the value of the reinvestment is divided by the tax-affected EBIT, i.e. net operating profit after taxes (NOPAT).

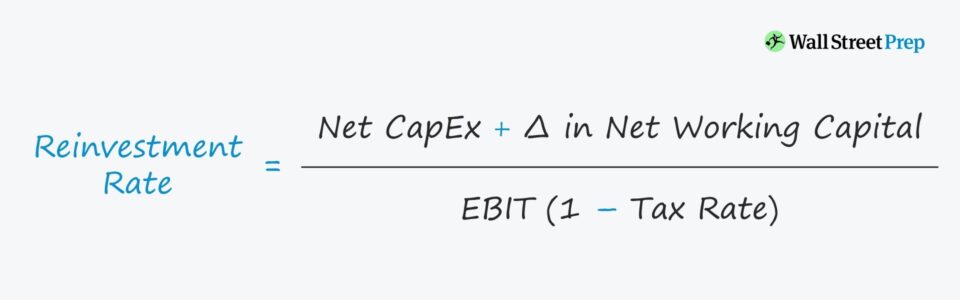

Reinvestment Rate Formula

The formula for calculating the reinvestment rate is equal to the sum of net Capex and change in NWC, divided by NOPAT.

Where:

- Net Capital Expenditure (Capex) = Capex – Depreciation

- NOPAT = EBIT × (1 – Tax Rate %)

What is a Good Reinvestment Rate?

The change in NWC is considered a reinvestment because the metric captures the minimum amount of cash necessary to sustain operations.

- Increase in Net Working Capital (NWC) ➝ Less Free Cash Flow (FCF)

- Decrease in Net Working Capital (NWC) ➝ More Free Cash Flow (FCF)

Note that the net working capital (NWC) calculation includes only operating items, and thereby excludes cash and cash equivalents, as well as debt and any related interest-bearing liabilities.

Why? Neither cash nor debt are operating items.

How Do Reinvestment Rate Impact Expected EBIT Growth?

Once calculated, the expected growth in operating income (EBIT) can be calculated by multiplying the rate of reinvestment by the return on invested capital (ROIC).

In practice, a company’s implied rate of reinvestment can be compared to that of industry peers, as well as a company’s own historical rates.

Companies with higher reinvestment activity should exhibit higher operating profit growth – albeit, the growth might require time to realize.

If a company consistently has an above-market rate of reinvestment, yet its growth lags behind peers, the takeaway is that the capital allocation strategy of the management team could be suboptimal.

While increased spending by a company can drive future growth, the strategy behind where the capital is being spent is just as important.

A clear trend of reduced reinvestment, in contrast, could simply mean that the company is more mature, as reinvestment opportunities tend to decline in the later stages of a company’s life cycle.

Learn More → Reinvestment Rate and Growth by Industry (Damodaran)

Reinvestment Rate Calculator | Excel Template

We’ll now move to a modeling exercise, which you can access by filling out the form below.

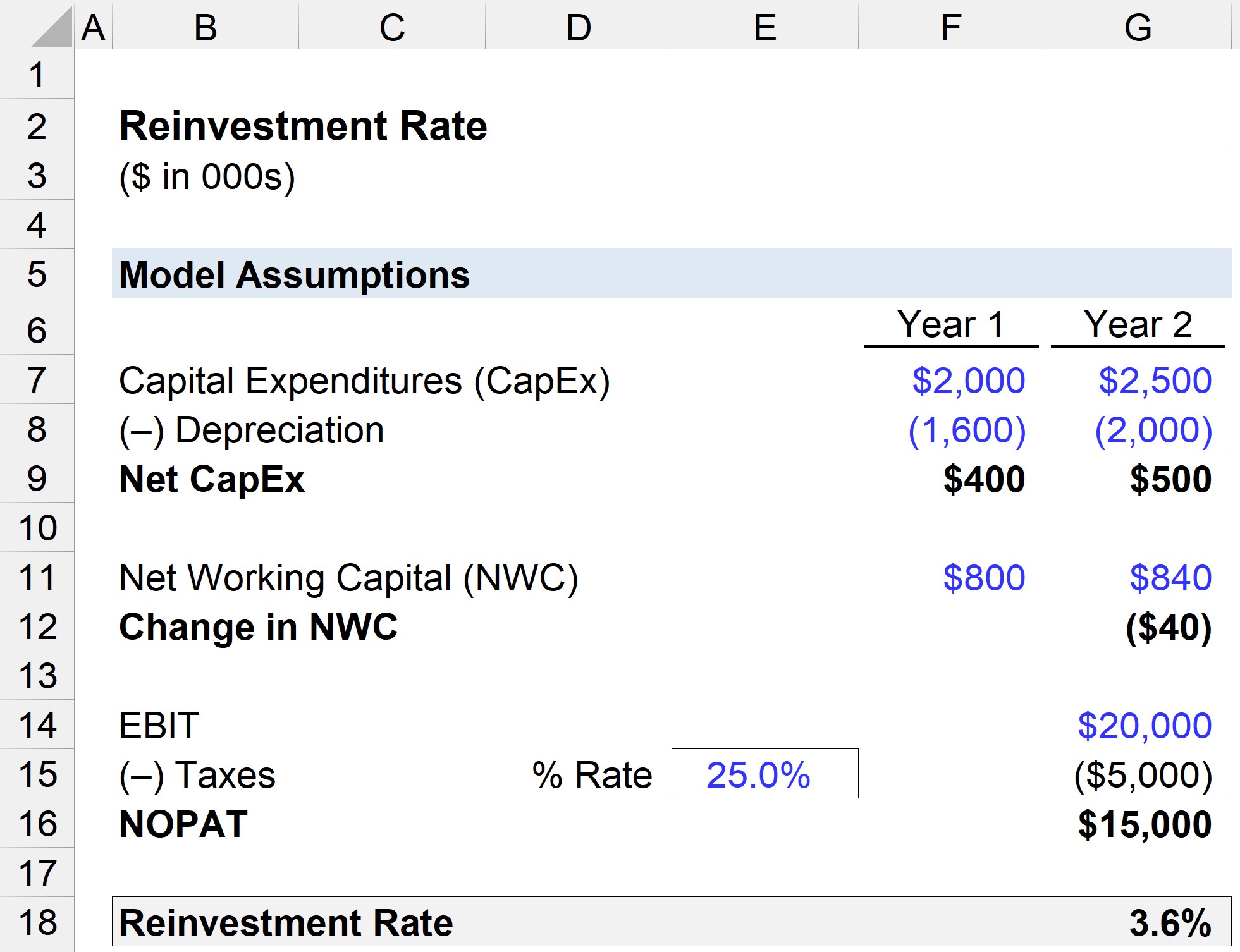

1. Capex, Depreciation and Working Capital Assumptions

Suppose we’re tasked with calculating the reinvestment rate of a company using the following assumptions.

Financials (Year 1)

- Capex = $2 million

- Depreciation = $1.6 million

- Net Working Capital (NWC) = $800k

Financials (Year 2)

- Capex = $2.5 million

- Depreciation = $2.0 million

- Net Working Capital (NWC) = $840k

From the financials listed above, we can reasonably assume the company is relatively mature, given how depreciation as a percentage of Capex is 80%.

If the company were unprofitable at the operating income line, using the reinvestment rate is not going to be feasible.

2. Reinvestment Rate Calculation Example

The change in NWC is equal to –$40k, which represents a cash outflow (“use” of cash), as more cash is tied up in operations.

- Change in Net Working Capital (NWC) = $800k Prior Year NWC – $840k Current Year NWC

- Change in NWC = ($40k)

Since a negative change in NWC is a cash “outflow,” the -$40k increases the reinvestment needs of our company.

With the numerator complete, the final step before arriving at our company’s rate of reinvestment is calculating the tax-affected EBIT, or “NOPAT”.

Here, we assume our company had $20 million in EBIT for Year 2, which at a 25% tax rate, results in $15 million of NOPAT.

In closing, the reinvestment rate of our company is 3.6%, which we calculated by dividing the sum of the net Capex and the change in NWC by NOPAT.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today

Hi, very detailed explanation!

Btw, can I check the reason for minus the depreciation from CAPEX?

Thanks!

Hi, Derek,

The reason is that some capex has to be allocated to maintaining the equipment the company already has, and this is taken to be the equivalent of depreciation; the remainder of capex is the ‘growth’ capex or the net reinvestment.

BB

Hi Brad, thank you so much for the explanation. However, may I ask would it be wrong to assume CAPEX allocated to maintaining equipment = depreciation? Afterall certain companies may decide to scrape its equipment at the end of its useful life instead of maintaining it.

Hi, Daryl, It may indeed be a reasonable assumption for a company that is merely maintaining existing equipment and selling the old equipment for salvage value, rather than investing in a growing base of equipment. In that case, there might still be a growth in capex due to inflation of… Read more »

Great post, I just want to if a company is showing more capex than its ebit for the past few years (like 300% or so), how can I know if its sustainable enough to forecast? and how it can be applied to a company which is in losses ?

Hi, Sakshi,

One of the limitations of this approach of understanding growth as a function of reinvestment and ROIC is that it does depend on sustainable and predictable ratios; it won’t make sense for an early stage company that has huge capex but is not yet profitable.

BB

What if a company is operating on negative working capital which is increasing year on year and their depreciation is more than net capex… resulted reinvestment of cash is negative…. results in a negative reinvestment rate or infinite

Hi, Mohammed, Negative working capital is possible for a growing business. However, depreciation being more than capex is not sustainable unless the business can run on zero PP&E, in which case depreciation would equal capex. However, it is possible that the amount of total operating assets in the denominator are… Read more »

Is it 3.6% or 3.06%?

Hi, Ramesh,

It is 3.6% (540 of net reinvestment divided by 15,000 of NOPAT).

BB

Hi, thank you fir the post!

How do you arrive at the expected growth rate equaling the product of ROIC and reinvestment rate? Thanks!

Hi, Alfred,

Using this approach, new income is a result of earning a return (ROIC) on new investment. So, if you take your reinvestment rate (% of historical income) and multiply it by the ROIC, you will get the growth in income. Does that make sense?

BB

Hi, thankyou for clarification, can you explain it brief as i am not connecting with with ROIC and Reinvestment rate and how it will give growth rate.

Thankyou for post, and this explanation. This explanation arises one question to me , as how these are related to growth as we have considered this year reinvestment rate and this year ROIC. When we reinvest today it will benefit in future not today, so why we taken this year… Read more »

Hi, Somya, The idea is that the return we earn on reinvested capital (ROIC is NOPAT / Invested Capital)) is what causes our NOPAT to grow. The ROIC is not necessarily just one year, but in general what kind of return we will earn on reinvestment, and we expect that… Read more »

Hello, nice work!!

I would like to ask; If the Change in WC were +40 instead of -40, would you add it to Net CAPEX or would you subtract it from the Net CAPEx?

Thanks

Thanks, Marcial! If the change in WC was positive, then it would be an addition to net reinvestment, and it would be modeled as a use of cash and reduction of free cash flow.

BB

Thanks for your reply. Then, it doesn’t matter if the change in WC is positive or negative it will always be added to net reinvestment,right?

Hi, Marcial,

Yes, any change in NWC is part of net investment, but if it is an addition to NWC, it is an increase in net investment and a use of cash, and vice versa for a reduction in NWC.

BB