Skip to main content

Skip to main content

What is Straight Line Depreciation?

Straight-Line Depreciation is the uniform reduction in the carrying value of a non-current fixed asset in equal installments across its useful life.

The straight-line method of depreciation assumes a constant depreciation rate, where the amount by which the fixed asset (PP&E) reduces per year remains consistent over the entire useful life.

How Does Straight Line Depreciation Work?

The straight-line depreciation method is characterized by the reduction in the carrying value of a fixed asset recorded on a company’s balance sheet in equal installments.

The process to calculate the annual depreciation expense under the straight line depreciation basis requires three variables:

- Purchase Price (Asset Cost) → The initial cost incurred to acquire the fixed asset (PP&E), i.e. the capital expenditure (Capex).

- Salvage Value → The residual value of the fixed asset (PP&E) at the end of its useful life, or “scrap value”.

- Useful Life → The number of years in which a fixed asset (PP&E) is expected to continue contributing positive economic benefits.

The concept of depreciation in financial reporting under U.S. GAAP (FASB) stems from the matching principle in accrual accounting.

Under the matching principle in accrual accounting, the costs associated with a non-current asset that’ll provide long-term benefits must be recognized in the same period for the sake of consistency.

Unlike current assets such as inventory, a fixed asset (PP&E), such as machinery, is expected to continue contributing positive economic value for more than one-year (>12 months).

Simply put, the depreciation expense can be thought of as the gradual decline in value of a fixed asset (PP&E) over its useful life assumption, which is the estimated duration in which a non-current fixed asset is expected to provide economic benefits.

Straight Line Depreciation Definition (Source: LII)

How to Calculate Straight Line Depreciation?

In the straight line method of depreciation, the value of the underlying fixed asset is reduced in equal installments each period until reaching the end of its useful life.

To calculate the straight line depreciation rate for a fixed asset, subtract the salvage value from the asset cost to compute the total depreciation expense.

Once determined, divide the total depreciation expense by the coinciding useful life assumption to arrive at the annual depreciation expense, which will be periodically recognized on the income statement.

The depreciation line item – which is embedded within either cost of goods sold (COGS) or operating expenses (OpEx) – is a non-cash expense.

Why? The real cash outflow occurred earlier on the original date of the capital expenditure (Capex).

Hence, the depreciation expense is treated as an add-back to net income on the cash flow statement (CFS), since no actual movement of cash occurred.

While there are a couple of other depreciation methods out there, the straight-line depreciation approach is by far the most common, namely because companies prefer the simplicity of the system and because accelerated depreciation causes a lower net income (and earnings per share, or “EPS”) in the near-term.

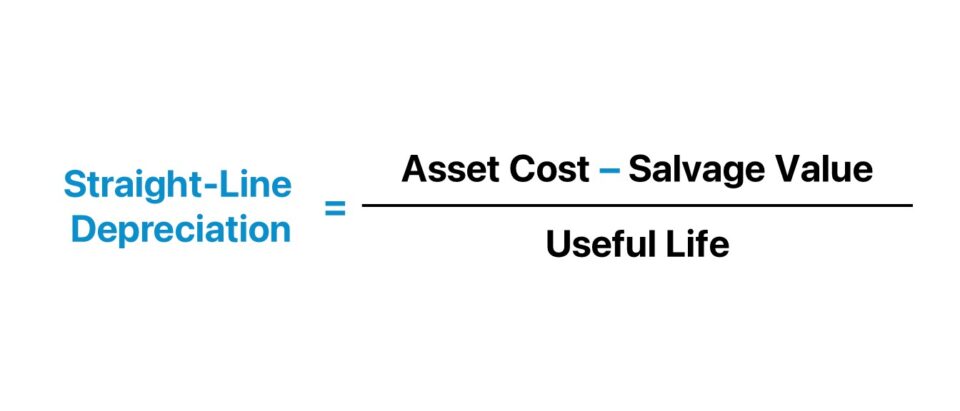

Straight Line Depreciation Formula

The formula to calculate the annual depreciation expense under the straight-line method consists of dividing the difference between the purchase price of the fixed asset (PP&E) and the anticipated salvage value at the end of its useful life by the total useful life assumption.

Where:

- Purchase Price → The total cost incurred by the company to acquire the fixed asset (PP&E)

- Salvage Value → The estimated value of the fixed asset at the end of its useful life. Usually, the salvage value is assumed to be zero because of the tax incentive (i.e. depreciation reduces pre-tax income on the income statement).

- Useful Life → The number of years that the fixed asset (PP&E) is expected to continue providing positive economic value to the company.

Straight Line Depreciation Calculator

We’ll now move to a modeling exercise, which you can access by filling out the form below.

Straight Line Depreciation Calculation Example

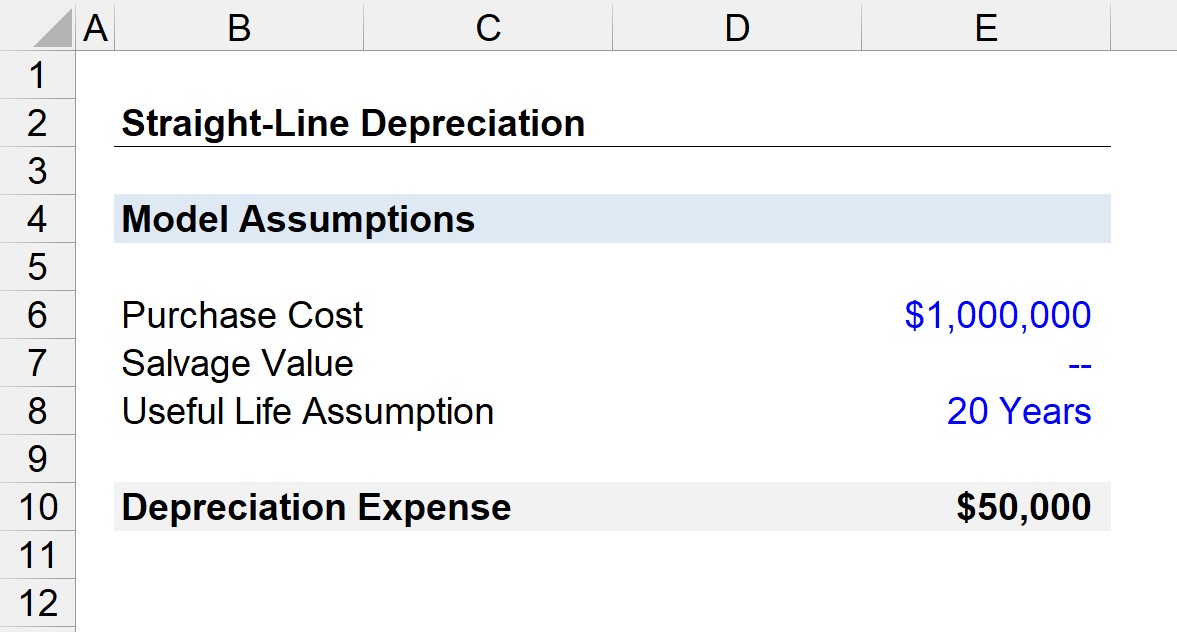

Suppose a hypothetical company recently incurred $1 million in capital expenditures (Capex) to purchase fixed assets.

Per guidance from management, the fixed assets have a useful life of 20 years, with an estimated salvage value of zero at the end of their useful life period.

- Purchase Cost = $1,000,000

- Useful Life = 20 Years

- Salvage Value = $0

In the next section, we’ll start by calculating the numerator, the purchase cost subtracted by the salvage value.

But since the salvage value is zero, the numerator is equivalent to the $1 million purchase cost.

After dividing the $1 million purchase cost by the 20-year useful life assumption, we arrive at $50k for the annual depreciation expense.

- Straight Line Depreciation Expense = $1 million ÷ 20 years = $50k

Therefore, the annual depreciation expense recognized on the income statement is $50k per year under the straight-line method of depreciation.

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today