Skip to main content

Skip to main content

What is the Depreciation Tax Shield?

The Depreciation Tax Shield refers to the tax savings caused from recording depreciation expense.

On the income statement, depreciation reduces a company’s earning before taxes (EBT) and the total taxes owed for book purposes.

How Does the Depreciation Tax Shield Work?

Under U.S. GAAP, depreciation reduces the book value of a company’s property, plant, and equipment (PP&E) over its estimated useful life.

Depreciation expense is an accrual accounting concept meant to “match” the timing of the fixed assets purchase—i.e. capital expenditure (Capex)—with the cash flow generated from fixed asset over a period of time.

The real cash outflow stemming from capital expenditures has already occurred, however in U.S. GAAP accounting, the expense is recorded and spread across multiple periods.

The recognition of depreciation causes a reduction to the pre-tax income (or earnings before taxes, “EBT”) for each period, thereby effectively creating a tax benefit.

Those tax savings represent the “depreciation tax shield”, which reduces the tax owed by a company for book purposes.

How to Calculate Depreciation Tax Shield

In order to calculate the depreciation tax shield, the first step is to find a company’s depreciation expense.

D&A is embedded within a company’s cost of goods sold (COGS) and operating expenses, so the recommended source to find the total value is the cash flow statement (CFS).

Once found, the next step is to copy the D&A value and then search for it in the search box, assuming that the amortization expense was combined with depreciation.

The actual separate depreciation value should be relatively straightforward to find within the SEC filings of the company (or if private, the specific amount might need to be requested from company management if not explicitly provided).

In the final step, the depreciation expense — typically an estimated amount based on historical spending (i.e. a percentage of Capex) and management guidance — is multiplied by the tax rate.

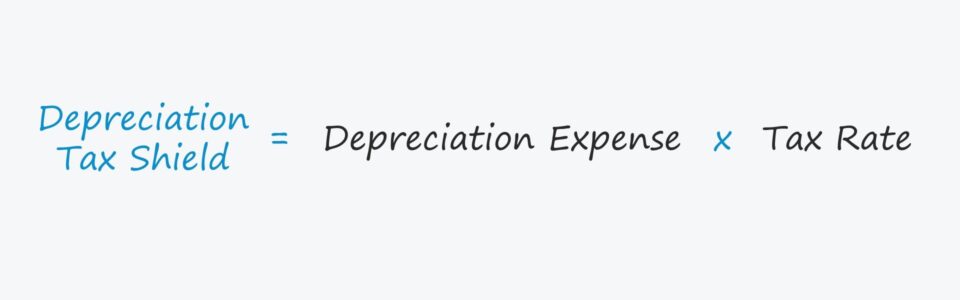

Depreciation Tax Shield Formula

The formula for calculating the depreciation tax shield is as follows.

If feasible, annual depreciation expense can be manually calculated by subtracting the salvage value (i.e. the remaining asset value at the end of its useful life) from the asset’s purchase price, which is subsequently divided by the estimated useful life of the fixed asset.

Because depreciation expense is treated as a non-cash add-back, it is added back to net income on the cash flow statement (CFS).

Therefore, depreciation is perceived as having a positive impact on the free cash flows (FCFs) of a company, which should theoretically increase its valuation.

Depreciation Tax Shield Calculator — Excel Template

We’ll now move to a modeling exercise, which you can access by filling out the form below.

Depreciation Tax Shield Calculation Example

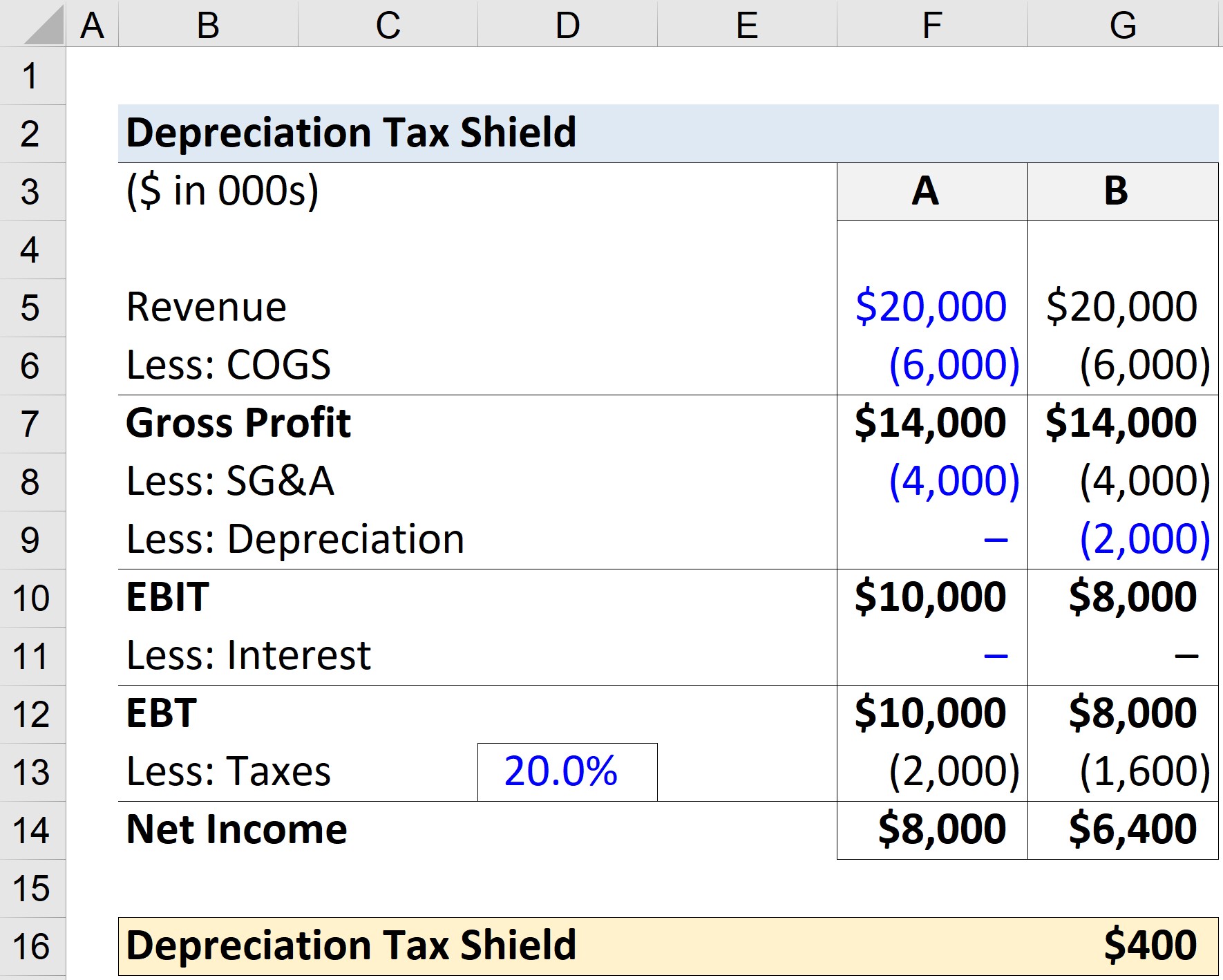

Suppose we are looking at a company under two different scenarios, where the only difference is the depreciation expense.

Under both scenarios — A and B — the financials of the company are as follows:

Income Statement Data

- Revenue = $20 million

- COGS = $6 million

- SG&A = $4 million

- Interest Expense = $0 million

- Tax Rate = 20%

Therefore, the company’s gross profit equals $14 million.

- Gross Profit = $20 million — $6 million

For Scenario A, the depreciation expense is set to be zero, whereas the annual depreciation is assumed to be $2 million under Scenario B.

Scenario A

- Depreciation = $0 million

- EBIT = $14 million – $4 million = $10 million

Scenario B

- Depreciation = $2 million

- EBIT = $14 million – $4 million – $2 million = $8 million

The difference in EBIT amounts to $2 million, entirely attributable to the depreciation expense.

Since we assume the interest expense to be zero, EBT equals EBIT.

As for the taxes owed, we’ll multiply EBT by our 20% tax rate assumption, and net income is equal to EBT subtracted by the tax.

Scenario A

- Taxes = $10 million * 20% = $2 million

- Net Income = $10 million – $2 million = $8 million

Scenario B

- Taxes = $8 million * 20% = $1.6 million

- Net Income = $8 million – $1.6 million = $6.4 million

In Scenario B, the taxes recorded for book purposes is $400k lower than under Scenario A, reflecting the depreciation tax shield.

- Depreciation Tax Shield = $2 million – $1.6 million = $400k

Everything You Need To Master Financial Modeling

Enroll in The Premium Package: Learn Financial Statement Modeling, DCF, M&A, LBO and Comps. The same training program used at top investment banks.

Enroll Today